Global financial markets are witnessing a powerful rally, with major indices reaching record highs as investors grow increasingly optimistic about both geopolitical developments and the strength of the U.S. economy. According to recent discussions on financial media, the ongoing war situation appears to be moving toward a resolution, and fears of extreme outcomes such as $200 oil prices or large-scale ground troop involvement are beginning to fade.

This shift in sentiment is playing a crucial role in driving markets higher. Analysts suggest that the market is effectively “looking through” the war, focusing instead on improving economic fundamentals and future growth expectations.

Strong Corporate Earnings Fuel Market Momentum

One of the biggest drivers behind the rally is robust corporate performance. Early earnings reports from S&P 500 companies indicate strong growth trends. Although only a small portion of companies have reported so far, revenue growth is already running at approximately 12.5%, significantly higher than the typical pace aligned with GDP growth.

Even more striking is earnings growth, which is currently up around 30%, exceeding expectations by roughly 10%. While these numbers may moderate as more companies report, early signals from financial and technology sectors suggest that corporate America remains in strong shape.

This surge in profitability reinforces a long-standing market principle: profits are the lifeblood of stock performance. With margins expected to remain high into next year, the outlook for equities remains supportive.

Record-Breaking Performance Across Indices

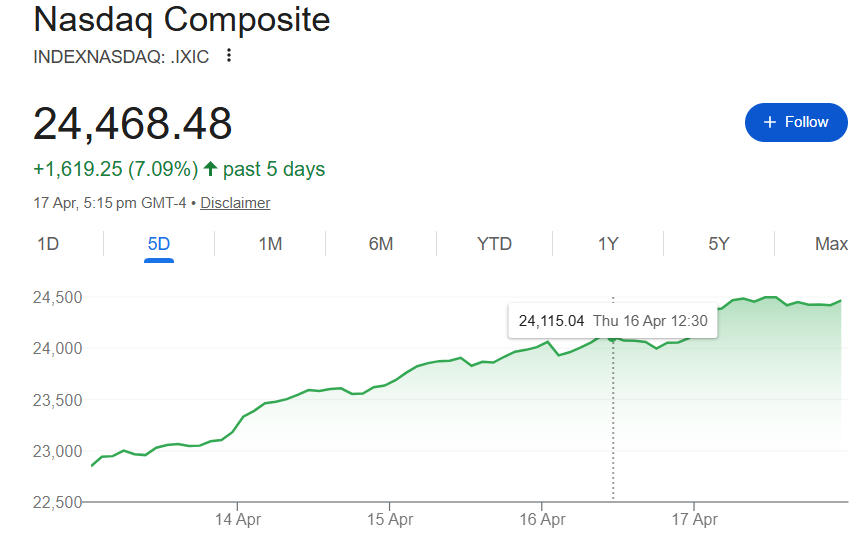

The rally is broad-based and historic in scale. The Nasdaq has recorded its best weekly performance since 1992, while the S&P 500 has surged above the 7,000 mark. Meanwhile, the Dow Jones is also climbing steadily, with projections suggesting it could approach 50,000 levels.

Such widespread strength indicates that the rally is not limited to a single sector but is instead driven by a combination of strong earnings, improving sentiment, and easing geopolitical risks.

Oil Prices and Energy Market Shift

Oil markets are also playing a key role in shaping the economic narrative. Prices have been declining, helping ease inflation concerns and supporting equity markets. Futures markets suggest oil prices stabilizing around $70 per barrel, which is considered sustainable for both consumers and producers.

In the U.S., energy production is becoming increasingly important on the global stage. Analysts highlight a structural shift in the global oil market, where reliance on the Middle East may decrease while American energy exports gain prominence. Countries across Asia, including Japan and China, are expected to rely more on U.S. supply.

However, production economics remain important. Surveys from the Dallas Federal Reserve indicate that producers in the Permian Basin require approximately $69 per barrel to justify drilling new wells, suggesting current price levels are balanced for continued output.

Consumer Strength and Tax Stimulus

Another key factor supporting the economy is rising consumer strength. Tax refunds have increased by 10% to 14%, injecting liquidity into households. A broader tax cut program worth around $100 billion, distributed across approximately 55 million people, is further boosting spending power.

Importantly, analysts note that oil prices would need to remain above $150 per barrel for several months before significantly impacting consumer behavior. Since such conditions have not materialized, discretionary spending remains largely unaffected.

Wage growth and strong employment trends are also contributing to higher disposable incomes, allowing consumers to absorb moderately higher energy costs without reducing spending.

GDP Concerns Remain Limited

Despite the strong momentum, there are some concerns. The Atlanta Federal Reserve’s real-time GDP tracker currently estimates growth at around 1.3%, which is below expectations. However, many analysts argue that this model has historically been volatile and unreliable, often compared to noisy job reports.

As a result, markets are largely ignoring this data point and focusing instead on stronger indicators such as earnings growth, consumer spending, and corporate investment.

Geopolitical Developments and Policy Impact

Geopolitical developments remain central to market sentiment. There is growing optimism that the conflict will conclude sooner than expected, reducing uncertainty. Donald Trump has been credited with pushing toward an end to the conflict, with expectations that improved global stability could boost economic confidence.

There is also discussion of coordinated efforts involving Gulf nations and NATO regarding key trade routes such as the Strait of Hormuz. However, recent statements suggest that the situation may already be stabilizing, reducing the need for further intervention.

At the same time, broader economic policy initiatives, including capital expenditure plans and corporate investments, are expected to drive growth in the second half of the year. Analysts describe the current phase as the beginning of a longer-term “bull market marathon,” supported by strong fundamentals and declining global risks.

Outlook: A Bull Market with Strong Foundations

Overall, the combination of easing geopolitical tensions, strong corporate earnings, stable oil prices, and supportive fiscal measures is creating a powerful backdrop for equities.

While uncertainties remain, particularly around GDP growth and global developments, the prevailing view among market participants is increasingly optimistic. Investors are betting that six months from now, economic conditions will be significantly better than today.

If current trends continue, global markets could remain on a sustained upward trajectory, marking one of the most resilient bull phases in recent history.

Disclaimer:

This article is for informational purposes only and should not be considered financial or investment advice. Readers are advised to consult a qualified financial advisor before making any investment decisions.